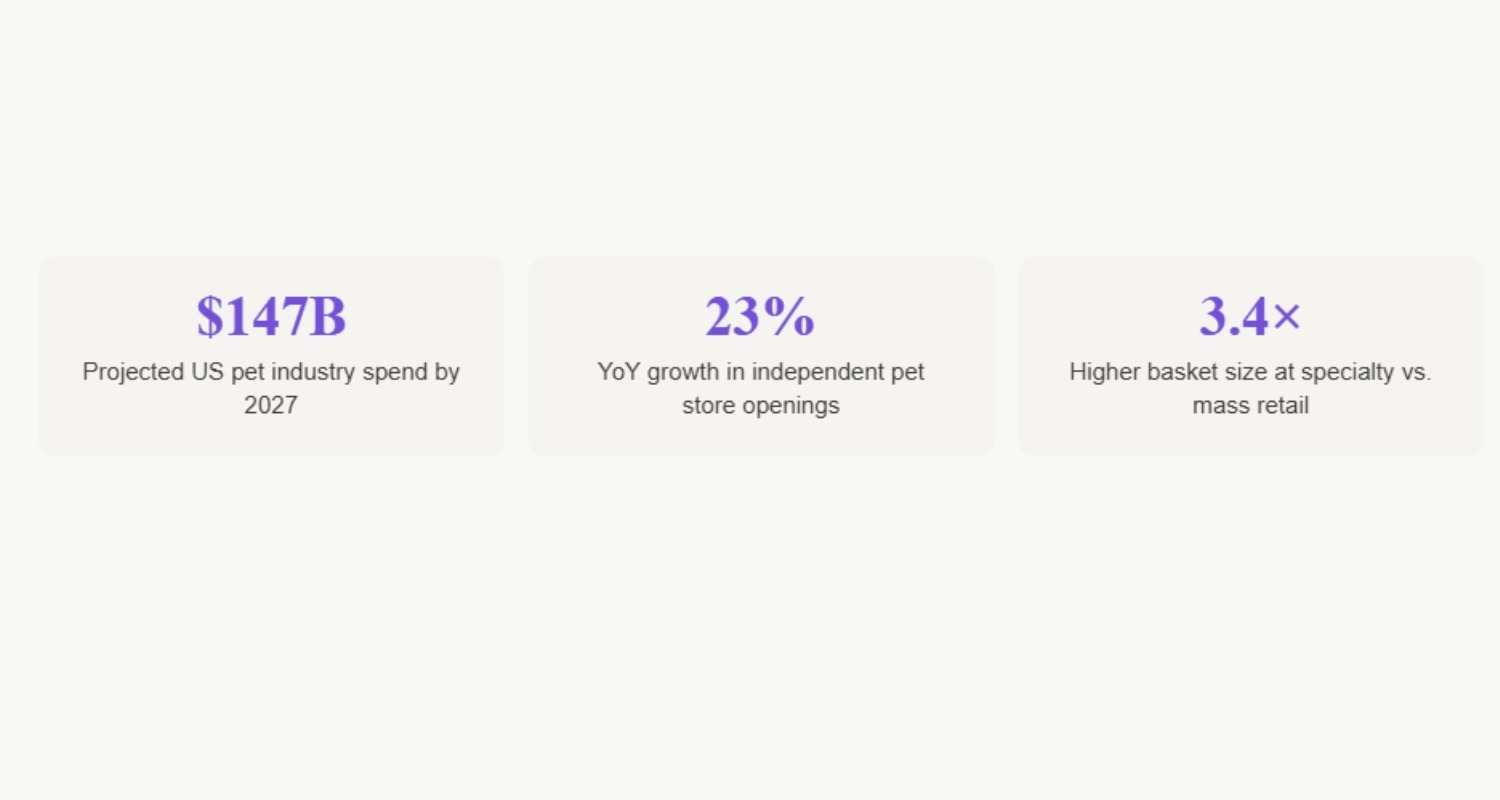

The pet industry has long been one of retail's most resilient sectors. Through economic downturns, shifting consumer habits, and the relentless march of e-commerce, Americans have kept spending on their pets, often outpacing growth in categories far more considered "essential." The result is a market that has ballooned well past the $100 billion mark and shows little sign of slowing.

But inside that growth story, a quieter revolution is underway. While national chains like PetSmart and Petco continue to dominate in total store count and revenue, a new class of independent pet specialty boutiques has emerged smaller, curated, community-rooted and they're finding their footing by competing differently. Not on price. Not in breadth. But on place.

Where Boutiques Are Winning — and Why It Matters

Location intelligence data paints a nuanced picture. Not all neighborhood types are created equal for the independent pet boutique, and the gap between a well-placed store and a poorly placed one is wider than most operators appreciate. MapZot.AI's foot traffic and trade area analysis points to several distinct positioning strategies that are generating outsized results.

Dense urban neighborhoods, particularly those with high concentrations of younger renters and working professionals show disproportionately strong pet boutique foot traffic. These are households where the pet-to-human ratio is high, discretionary spending on premiumization is established, and walkability turns a pet supply run into a social ritual rather than a chore.

Emerging suburban corridors are a second hotspot, particularly in markets that have experienced post-pandemic population inflows. As families relocated from urban cores to inner-ring suburbs, they brought their spending behaviors with them including a preference for premium, specialized pet retail over mass-market alternatives.

The Chain Advantage — and Its Limits

It would be a mistake to underestimate the national chains. PetSmart and Petco combined operate thousands of locations across the country, and their real estate teams have spent decades optimizing for high-traffic suburban strip centers, often co-anchored with grocery or home improvement tenants. That model generates reliable foot traffic and strong brand awareness.

But the chains' greatest strength is also their greatest constraint. Strip mall formats and suburban power centers are increasingly the wrong address for a meaningful share of the pet-spending population. Urban density, mixed-use development, and walkable main streets the formats where boutiques thrive remain largely inaccessible to box-format operators. Their real estate playbook simply doesn't extend there.

This geographic asymmetry is the single biggest structural advantage independent boutiques possess. They can go where the chains cannot or will not.

Five Factors That Separate High-Performing Boutiques

Across the stores showing the strongest foot traffic retention and visit frequency, several location-driven factors appear consistently:

Proximity to complementary pet services. Stores within a walkable radius of groomers, daycares, vets, and dog parks benefit from natural cross-traffic. Pet owners in errand mode are already primed to spend.

Neighborhood lifestyle alignment. The most successful boutiques sit in areas where the surrounding retail mix specialty food, fitness studios, coffee shops signals the same premium, lifestyle-oriented consumer. Context matters.

High daytime population density. Independent stores that capture both morning dog-walk traffic and midday errand visits perform significantly better than those reliant on a single visit window.

Minimal direct chain overlap. Trade areas where the nearest big-box pet retailer is two or more miles away show stronger loyalty metrics for independents. Distance from the chains isn't just convenient, it's protective.

Strong residential anchors within one mile. Boutiques that serve a dense, stable residential base apartments, townhomes, single-family neighborhoods with high pet ownership rates build the repeat visit cadence that drives profitability.

International Visitors Are Choosing Camping, Too

One of the more notable dimensions of the 2026 camping surge is its international character. Visitors from Mexico, South America, and Europe groups that have historically leaned toward hotel accommodations to anchor a more conventional travel itinerary are now showing up in the campgrounds. For many, it started as a cost calculation and became something more. The campground functions as a self-contained community: multilingual, multicultural, and increasingly appealing to travelers who came for the music but stayed for the social experience.

This has important implications for how brands and businesses position themselves around the festival. The Coachella camper in 2026 is not a niche demographic. They are domestic and international, first-time and repeat, budget-motivated and experientially motivated. Their spending behaviors reflect that breadth.

What the Data Suggests About Market White Space

One of the more striking findings from MapZot.AI's trade area modeling is how much genuine white space still exists in the independent pet boutique market. Despite the apparent density of pet retail options in many metro areas, large segments of the premium pet-owning population remain underserved too far from the nearest independent boutique, too discerning for the chains, and too habitual in their spending to be fully captured by e-commerce.

These pockets of underserved demand are disproportionately concentrated in gentrifying urban neighborhoods, emerging mixed-use suburban town centers, and secondary metros that have absorbed post-pandemic migration. For operators willing to do the location analysis, the opportunity is real and, in many markets, not yet crowded.